Annual figures 2019

The consolidated financial statements of SD Worx NV for the year ended 31 December 2019 have been prepared in accordance with Belgian Generally Accepted Accounting Principles (BE GAAP). The group’s consolidated financial statements have been audited by Deloitte (unqualified opinion). Regulated information.

Overview definitions

SD Worx NV presents its results in accordance with generally accepted accounting principles in Belgium (“BE GAAP”).

Alternative performance measures (“APMs”) present useful information which supplements the group’s financial statements and which allow the reader of the financial statements to better understand the financial state of the group and the wider group. These measures are not defined under BE GAAP and may not be directly comparable with APMs for other companies. The APMs represent important measures for how management monitors the company and its business activity. The APMs are not intended to be a substitute for, or superior to, any BE GAAP measures of performance. Some of the financial information presented in our annual reports contains APMs. These include Normalised EBITDA and Consolidated net result excl amortisations and impact of changes in actuarial assumptions. Below we define these APMs and reconcile them with BE GAAP measures.

“EBITDA” means Earnings Before Interest, Taxes, Depreciation and Amortisation, or operating result profit (loss) (code 9901 of the BE GAAP consolidated financial statements) before charges for fixed asset depreciation, amortisation and impairment (code 630 of the BE GAAP consolidated financial statements).

(As an explanation for the use of this APM, EBITDA provides an analysis of the operating results, excluding depreciation and amortisation, as they are non-cash variables which can vary substantially from company to company depending on accounting policies and the accounting value of the assets. Additionally, it is an APM which is widely used by investors when evaluating businesses (multiples valuation), as well as by rating agencies and creditors.)

“Normalizations” means the revenues and expenses of which, in case of a change of control, an acquirer has the choice or option (mid- or long-term) to not realise those revenues or incur those expenses. In other wordt, expenses or revenues which are not part of the recurring business operations of the SD Worx group.

“Normalized EBITDA” is determined as EBITDA before (a) restructuring & integration costs, (b) business and asset disposals, (c) acquisition & transaction costs related to third parties, (d) profit or loss from discontinued operations, (e) share-based compensation, (f) other non-operating income/expense below the line, and (g) digital transformation initiatives - one-off investments.

(As an explanation for the use of this APM, Normalised EBITDA is used to provide insight in the recurring level of operational profitability. Please also refer to the definition of Normalisations below.)

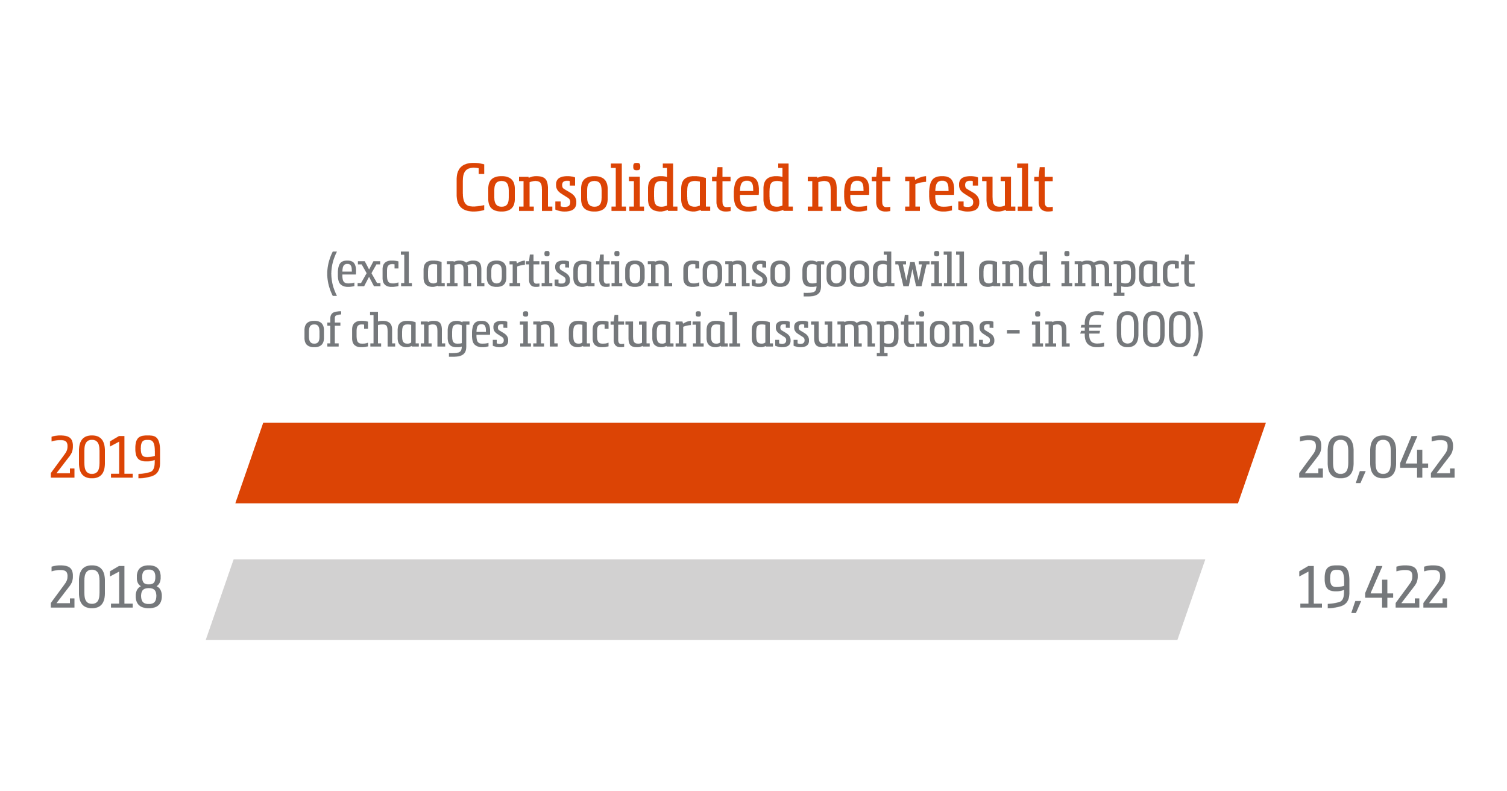

“Consolidated net result excl amortisations and impact of changes in actuarial assumptions” is determined as the consolidated net result before (a) the amortization of consolidation goodwill and (b) the after tax impact of changes in IAS19R Employee Benefits – impact of changes in actuarial assumptions.

(As an explanation for the use of this APM, Consolidated net result excl amortisations and impact of changes in actuarial assumptions is used to provide a high level insight in the net result if the results were presented in IFRS instead of BE GAAP. In IFRS, the non-cash expenses related to IAS 19R impact of changes in actuarial assumptions are reported in Other Comprehensive Income and goodwill is assumed to have an indefinite useful life, whereas in BE GAAP it is amortized on a straight-line basis.)

For an overview of the normalisations per financial year and reconciliation with operational profits, we refer to Note 15. Non-recurring items and normalizations.